This article is for educational and entertainment purposes only. This is not legal advice and should not be relied on as such. Every case is different. Consult a licensed professional in your state. Viewing this website or its content does not create an attorney-client relationship with Lyda Law Firm or any of its lawyers.

Thinking about starting a business? Or maybe you’ve already got the ball rolling with your startup, but want to make sure you’re doing it the right way?

Great! This series is for you.

Our 16-Step Legal Checklist for Startups & Small Businesses walks through starting a business step-by-step. We start in the pre-planning phase and cover everything from setting your goals and writing a mission statement all the way up to defining your liabilities and drafting your legal contracts.

We don’t just look at it from an entrepreneurial perspective, we look at it from a legal perspective. It is important to adopt a legal mindset when starting a business because you need to protect yourself in case of a lawsuit.

Creating a clearly defined mission statement is the first thing you should do when starting a business or entrepreneurial venture.

There are many resources that go into great depth about writing a mission statement, but it’s ultimately a very personal process. If you want to read a whole book on the subject, Start With Why by Simon Sinek is a popular resource.

To come up with your mission statement, start with reflection. Ask yourself these important questions and reflect deeply.

After you’ve gone through the reflection phase, articulate your findings. Grab a pen and paper and write down some of the answers you developed during reflection. Your mission statement is not something that just lives in your head. Actually write it down and read it back to yourself. Then revise it. Then revise it again.

There are no formal requirements for what a mission statement has to say or include. It can be short or it can be long. The important thing is that it clearly communicates what is driving you to start this particular business. The whole purpose of a mission statement is to communicate your business’s purpose to yourself and to others.

But why is a mission statement included in a legal checklist?

We included this step because Your mission statement will act as your north star and guide your later legal decisions. It will inform the type of entity you select, your tax treatment, who you work with, where you work, and more. We will discuss those particular decisions in future chapters.

At the Lyda Law Firm, our mission statement is to:

“Increase access to high-quality legal services for small businesses and moderate-income individuals.”

Each word in our mission statement was carefully selected. We don’t just want to provide legal services, we want to provide high-quality legal services. We want to increase access, meaning we want to make legal services more affordable. We also have a focus on our clients: small businesses and moderate-income individuals - these two demographics are often underserved in the legal industry.

One thing to keep in mind about mission statements: even though they are your north star in guiding your business, they are not necessarily set in stone. Your mission statement can evolve as your business evolves.

For example, we’ve realized that the Lyda Law Firm’s mission statement does not address something important to us: how we treat our employees. The legal industry has an incredibly high burnout rate, so it’s important for us to create a positive work environment for everyone on the team. We have not yet incorporated that into our mission statement and that is one way we expect our mission statement to evolve.

Once you’ve successfully defined your mission, it’s time to start looking into the future.

Once you’ve set a clear mission statement, it’s time to look into the future of your business and define your end goal.

Defining your end goal is slightly different from defining your mission statement. It’s more specific and it’s more concrete.

Picture your business in one year, five years, ten years, and at the end of your career. Where do you see your business down the road?

It might seem too early to think about your exit, but defining your end goal will affect all of your later legal decisions.

For example, if you want your business to become publicly traded, you likely to want to set yourself up as a C-corp (a subchapter C corporation) right from the get-go (we’ll go into more details about selecting an entity type in future chapters).

Another example of how your end goal can have legal impacts on your business is if your end goal differs from your business partner. If that’s the case, you could face legal complications down the road.

Your end goal will also affect where you do business and even what state you register your business in. There are advantages to registering in different states, but those advantages are only worth it if you have a specific end goal in mind. For example, registering a business in Delaware can be advantageous for large corporations, but it probably doesn’t make sense for a small local business.

That main point is that there are many legal decisions that will ultimately trackback to your end goal.

All of those are legitimate end goals for a business. No one end goal is better than the other. It’s just important to find out what works for you and your future so that you can have that as a baseline for all of your legal decisions going forward.

Next up in the Legal Checklist for Startups, we’ll discuss why it’s important to define the people associated with your business.

The next step to think about when starting your business is what we call “defining your who.” This is when you identify the people who will be involved with your business.

Like some of the other items on this list (like defining your mission and defining your end goal), defining your who is not in itself a legal concept, but it will absolutely affect your legal decisions.

The “who” of your business can be broken down into three different parts:

Let’s take a look at each of these parts in more detail.

The first group of people you should identify is potential partners.

We talked about this earlier in Defining Your End Goal. If you’re thinking about going into business with a partner, it’s important that you both have a similar end goal. Otherwise, you could go off in different directions, which could create a lot of tension.

You’ll also want to make sure that a partnership is right for you, personally. If you are considering bringing on a partner, make sure you are comfortable giving up some level of control. Also try to identify what each of you brings to the table so you can break up responsibilities and set realistic expectations.

The next group you need to think about when defining your who is people who will work for your business. Namely, employees and independent contractors.

It is extremely common for businesses to pay their workers as independent contractors when they should be treated as employees. If you try to save tax money by classifying an employee as an independent contractor, it can come back and bite you. If you are caught, you’ll have to pay back-taxes and penalties.

In short, if you have someone who is working for you most of the time, and your business mostly supervises them and the time, place, and manner of their work; then they are most correctly and appropriately defined employees rather than independent contractors.

When you are thinking of who will work for your business, think about the day-to-day activities that you can’t (or don’t want to) handle. Next, think if this will be a person who you will bring on full or part-time as an employee, or if this can be handled by a contractor (or a combination of the two).

Another group to think about when you are defining your who is other collaborators.

One of the most significant types of collaborators are lenders and investors. If you collaborate with people who will be providing funding for your business, you need to think about what type of relationship you want. At this stage, you may not know specifically who your investors will be, but you can start to think about what types of investors you would want.

For example, if you’re seeking venture capital funding, do you want an investor who just gives you money and gets out of the way? Or do you want someone who will serve more as a mentor and advisor to your business, with a board of directors seat and hands-on involvement in the day to day operations?

The last group we will talk about in defining your who is vendors. Vendors could be the suppliers of raw materials, landlords, service providers (such as advisors like attorneys and accountants), and even technology providers. Vendors are much like independent contractors or employees, but instead of being individuals, they are most often other businesses.

When considering outside collaborators, think about your strengths and weaknesses. What skills are you lacking? Does it make sense for someone (a partner, employee, or other collaborator) to fill that gap?

Why is this important? Because if you bring on partners it will affect the type of business entity you select. If you have people working for your business it will affect your tax decisions. Keep reading, because we will discuss business entities and tax treatments in future sections.

Item #4 in the Legal Checklist for Startups is to define your “where.” This doesn’t just mean figuring out what state you want to work in, there are more intricate details that you’ll have to work your way through.

You “where” can be broken down into three parts.

Let’s take a look at each part in more detail.

First, where do you want to work? We’re not just talking about what city or state you want to work, we’re talking about your specific location. The main options here include retail space or office space.

If you are selling hard goods, then you will more than likely need a retail space. Operating your business out of a retail space opens up your business to potential liabilities if someone gets injured in your store, so you’ll want to make sure proper legal protections, like insurance, are in place.

You’ll also need to think about a commercial lease and negotiating that lease. Another factor that you’ll obviously need to consider for any retail location is advantages and disadvantages of that space. For instance, do you want to be in a location with a lot of pedestrian foot traffic? If so, monthly rent will probably be much higher than a place that is off the beaten path.

When selecting a retail space, it is important to weigh the pros and cons and estimate the eventual impact on your business.

If you are in the service business or another profession industry, you may not need a retail space and opt for an office space instead. There are a few factors to consider when selecting an office space that will affect your legal and financial decisions.

For instance, do you need a space for a large group, or just a few key individuals? How much do you want to grow your team? This is a decision that will be affected by defining your who, which we talked about in the previous section.

If you’re going to have an office, will a virtual office suffice? Virtual offices can be a great way to keep expenses low while maintaining the benefits of a physical office space. A virtual office is a place where you can receive mail or rent out conference space while working remotely from your home or other office location.

Speaking of other office locations, coworking spaces are growing in popularity. Coworking spaces can offer a great environment for collaboration and can lead to random interactions with other small businesses. Many coworking spaces also have private offices within the larger coworking space, so you can have the privacy of a personal office with the benefits of a coworking space.

If you do want your own private office, you need to consider potential liabilities if someone is injured at your office. You’ll also have a commercial real estate lease to consider. If you have a long-term commercial real estate lease, it is not uncommon for landlords to ask for a personal guarantee, especially for new business owners. If your landlord requires a personal guarantee, it is imperative that you fully understand the agreement and what it means for your personal finances.

The second part in defining your where is figuring out in which state you want to register your business.

We previously mentioned that if you are interested in starting a large corporation that you may want to register in Delaware. Many businesses register in the state of Delaware because of their specialized business courts and other advantages for large corporations. But if you have no intentions of growing that large, you may not need to go through all the trouble to register in a different state. Registering in your own state is likely to be perfectly sufficient.

In most instances, registering in the state where you live and work makes the most sense. But with all major business decisions, it is never a bad idea to consult with a professional.

We will talk about how to register your business in Step 8.

The third part of defining your where is to determine where your customers are. If you are a small retail business, your customers may only be in your state. But it is becoming more and more common for businesses to interact with customers in other states and even in other countries.

If you are selling a product or service across state lines, you could become subject to the laws of those other jurisdictions.

For example, if you’re selling a product out of Colorado to people in other states, there is a possibility that you could get sued in those other states because you’re choosing to do business in those states. The law will say you’re purposefully availing yourself of business contacts in those other states.

We’ll later talk about determining your industry-specific regulations. If you’re doing national or international business, you’ll need to think about how laws in those areas could potentially affect your business.

That wraps up Step 4 in the Legal Checklist for Startups: determine your “where.” Next up, we’ll talk about how you can protect your brand and intellectual property.

The first four steps in the Legal Checklist for Startups included a lot of big-picture thinking. While all of these things are important and will affect your legal decisions down the road, none of them are specifically attached to a legal concept.

That all changes with step number five, which is protecting your brand and your intellectual property.

Intellectual property is one of the most important legal issues any new small business faces. It’s also one of the most misunderstood areas of the law.

So what is intellectual property?

Intellectual property, or IP, is any unique creation of your own mind that the law protects from being stolen.

That’s right, the law will actually protect you from having your ideas, or the creations that come from your ideas, from being stolen by other businesses.

The law offers three main types of protection for your intellectual property:

But before we dive into each of these types of protection, let’s quickly discuss some common misconceptions about IP protection.

The most common misconception about intellectual property is that you have no protection unless you actually register for a trademark, copyright, or patent.

That’s not the case. In fact, your ideas are protected by common law even if you do not register for a trademark, copyright, or patent.

However, it can be much more difficult to prove something is actually your intellectual property unless you have some sort of legal protection. For instance, someone could claim that came up with a name or idea before you. Plus, you can only receive statutory rewards in a lawsuit if you have actually registered for intellectual property protection.

Ultimately, it is prudent to protect yourself and your business by registering for intellectual property protection.

Many states offer some level of intellectual property protection, but the most common way to protect yourself is by registering for intellectual property protection with the U.S. Patent and Trademark Office - the USPTO.

So let’s talk about each of the three categories of protection: trademarks, copyrights, and patents.

A trademark is something that usually protects the name or the logo of your business.

If your business is called XYZ Corp., you could register a trademark so that nobody else can start a business called XYZ Corp. in your specific line of work.

It is important to highlight trademarks are only specific to your line of work. The USPTO has separate “classes” and your trademark is only applicable within that class. For a full list of classes directly from the USPTO, visit this page.

For example, if you are an auto mechanic and you want to be called XYZ Auto Mechanic, you can register for a trademark in Class 37(Construction and repair). But that doesn’t mean a company can’t register for a trademark for its line of beauty products called XYZ Beauty Products in Class 3 (Cosmetics and cleaning products).

If your business offers several different products and/services, or you think it overlaps between categories, you can often register for a trademark for several categories. Keep in mind, you will have to pay a filing fee for each separate class.

As mentioned above, trademarks can not only protect the name of your business, but also how your business name is written and visually represented. That could include a specific font, style, and color; or the actual logo for your business.

On the USPTO’s website, you can register for a trademark (even without the help of a lawyer). When you register a trademark, you will have to pay a filing fee. Trademark filing fees vary and are calculated on a “per class basis.”

The second type of protection for your intellectual property is copyrights. Copyright traditionally protects things like the written word. If you write a book, you have a copyright on that book.

One of the most prominent uses of copyright law, especially for startups, is to protect computer code. If you are a tech computer or a software company, it is imperative that you protect your proprietary computer code with some sort of intellectual property protection.

A patent is another option to protect computer code, but the emerging trend is for copyright law to actually govern and protect any code you write.

The two basic requirements for copyright protection are (1) fixation, and (2) originality. So to be copyrightable, it must be an original work of authorship, and fixed in a tangible medium of expression. Technically, registration is a legal formality, and you can have a protected work without registering, but you can't assert a civil claim for copyright infringement against someone else unless you have registered. And, with a few exceptions, you can't get an award of statutory damages or attorney's fees without registration.

The third type of intellectual property protection is a patent. Patents are typically used for scientific or technological innovations.

In order to receive patent protection, a specialized lawyer will need to file for the patent for you. In order to represent you in what’s “called prosecuting a patent” lawyers not only have to pass the bar exam, they also have to pass the patent bar exam. And in order to do that, your lawyer would need to have a scientific background before going to law school.

If you are looking for protection for scientific or technological advancement, a patent may be the way to go. To get started, contact a qualified attorney in your state.

Intellectual property protection is such an important issue for small business owners because often times your intellectual property is the most valuable thing your business owns. If you have any doubt about what type of protection to seek, or how to seek it, consult with an attorney.

This section just scratches the service of intellectual property law. We’ll make sure to revisit this topic in other articles.

Next up, we’ll talk about funding your startup.

We’ve all heard the saying, “It takes money to make money.” And in the case of most startups and small businesses, it’s true. You are going to need some amount of money to start your business. Initial startup costs can range from a couple of hundred dollars for single-person businesses, to hundreds of thousands of dollars for big tech startups and brick and mortar stores.

In this section of the Legal Checklist for Startups, we’re going to walk through the various methods you can use to fund your business, plus provide some insights into the potential pros and cons of each.

The three main ways to fund a new business are:

Let’s look at each one individually.

Self-funding is the simplest and cleanest way to fund a new business venture. When self-funding, you don’t have to pay any interest (like you would with a loan) and you don’t have to hand over any control or ownership (like you would with outside investors).

As a self-funding business, you are in the driver’s seat.

The biggest obstacle to self-funding is, obviously, having the available capital. Another issue is that self-funding could limit how quickly you expand, which could lead to missed opportunities.

If you have enough cash on hand to avoid these pitfalls, self-funding is the smoothest path forward.

When it comes to self-funding (and all other forms of funding), it is imperative that you separate your personal and business expenses. We’ll talk more about that in Step 11: Create a Separate Bank Account. Also, it may be helpful to consult with an accountant to determine the best ways to use your own funds.

The second way to fund your business is through a loan.

There are several different types of loans for small businesses. The most well-known is an SBA loan, which stands for Small Business Administration loan.

SBA loans are guaranteed up to a certain point by the federal government. This means that lenders can give them out with good interest rates because they have a high level of confidence that they will be paid back. If the lender can’t get the money back from you, they can get a certain amount back from the government.

One common and very dangerous misconception about SBA loans is that if you are not able to pay it back, you will get off scot-free because the government will cover you. This is not the case, the bank will still come after you. Only after the lender exhausts all collection efforts will the government step in. The banks will get their money, and they will most likely get it from you.

The major downside of SBA loans is that they are very hard to qualify for. You have to have excellent financials, excellent credit, and you might even have to put up collateral (such as your home) as part of the loan.

If you don’t qualify for an SBA loan, there are many different types of private loans to fund your business that are not backed by the government. Since they do not have a government guarantee, they usually have higher interest rates.

The downside of any loan (personal or professional) is that you have to pay it back (with interest). That means that your business will owe monthly, quarterly, or annual payments to the lender. Repayment schedules for small business loans vary. Repayment typically starts one or more years after the start of the loan and can last a few years or a few decades depending on the loan amount.

If you’re unable to pay back a loan, the lender can attempt to collect on the debt that you owe. Collection methods vary from state to state, so consult with a professional in your state and make sure you understand the consequences of delinquent payments. Also, make sure you understand who is liable to make those payments. Depending on your business entity type, your personal assets could be at stake (we’ll talk more about that in the next section).

The third way to fund your business is through outside investors. It’s important to make this decision early because if you use outside investors, you should consider forming your business as a subchapter C corporation, also known as a C corp.

There are a lot of factors to think about when considering outside investors.

First, how many investors do you want? With every new investor comes a new chef in the kitchen. For instance, venture capital investors often want a seat on your board of directors, meaning they’ll oversee your job and essential be your boss.

Think long and hard about whether those investment funds are worth giving up control over your business.

The flip side of that argument is that having a sophisticated member of your board of directors could be a great mentorship opportunity for you. It can be a great way to learn from their experiences and to seek guidance for your business.

Also, if you bring on investors, it typically means handing over shares of your business in exchange for capital, making the investors partial owners of your business.

There are also a host of laws and regulations governing outside investments in your business. If you go this route, do your homework and consult with a securities lawyer licensed in your state.

Now that we’ve talked about the three main ways to fund a business, remember that you can do some combination of all three. You can self-fund a portion of your business and make up the remainder through loans and investors.

Next, let’s dive into the various business entities you can choose from.

Selecting your type of business entity is one of the most crucial early decisions for all small business owners.

The business entity is the legal structure of your business. This decision determines, among other things, (1) how the government taxes your business, (2) how your assets are protected (or not protected) in a lawsuit, and (3) what types of investments you can accept for your business.

Many of the previous sections have been building up to this decision. We talked about defining your “who,” defining your “where,” and planning your funding... all of those earlier decisions now come to fruition with selecting your type of entity.

Here are the basic entity types that are generally available in most states:

Let’s walk through each one to help you decide which is best for your business.

A sole proprietorship is the most basic type of business entity.

In a sole proprietorship, you are the only person in charge of your business and you have no liability protection. That means that if you get sued, your personal assets are on the line and there's really nothing protecting you.

One of the benefits of a sole proprietorship is that there is no double taxation. In other words, you don't get taxed at the business level and at the individual level. Another benefit is that it is very easy to set up.

Sole proprietorships are a very basic way to set up a business. Legally speaking, this is the equivalent of not setting up your business at all. It’s really an old fashioned way to do business. If you’re serious about the future of your startup, you will more than likely want to consider another option.

The second common type of business entity is a corporation. In many ways, this is the polar opposite of a sole proprietorship. With a corporation you have liability protection, meaning that if you are sued for negligence or breach of contract, you generally have a level of protection of your own personal assets.

One of the downsides of corporations is that there are all sorts of corporate formalities and extra paperwork. Plus, traditional corporations are typically double-taxed. That means you are taxed at the corporate level and at the individual level. That particular type of corporation is called a subchapter C corporation, commonly known as a C corp.

There is a more recent development called a subchapter S corporation, which is like a C corp except that it has pass-through taxation, meaning you are generally taxed at the individual level and the IRS does not tax you at the corporate level. So that's a little bit of the best of both worlds.

On the other hand, a C corporation has greater flexibility in the number and type of investors it can use for funding the business. So, if you are planning on seeking venture capital or even hope to be publicly traded someday, you might consider a C corporation. As with so many other decisions, it all depends on your end goal.

Speaking of the best of both worlds, there is also something called a limited liability company (LLC) This is a state law concept available in many, if not all, states.

LLCs provide liability protection and pass-through taxation. LLCs are becoming a more and more common way to organize your business. They are not as complicated as corporations, and they do not have the double taxation that you see with a C corp. And they also won’t leave you completely vulnerable as a sole proprietorship would.

If you do not intend to take on a large number of investors or seek investments from companies or foreign nationals, an LLC is frequently the way to go. Again, keep your end goal in mind as you make this decision.

There are also partnerships. The first two types of partnerships that we’ll talk about are designed for equal partners, meaning that everything (responsibilities, liabilities, benefits, etc.) is split equally.

First is the oldest traditional way of doing a partnership, called a general partnership. This is the partnership equivalent of having a sole proprietorship. That means that both partners are completely in charge of liabilities.

There is also something called a limited liability partnership (LLP). It is like a general partnership in that both partners are in it together and there is no differentiation between the levels of responsibility and benefits. The benefit of a limited liability partnership over a general partnership is limited liability, of course.

You may want to set up a partnership where the partners have differentiated levels of responsibility and benefit. Those are called limited partnerships. In a limited partnership, you have a general partner who is in front, doing the work, taking on the responsibility; and you have a limited partner, sometimes these are just investors backing the business but don’t want to be involved in the day-to-day operations

A limited partnership (LP), is the basic way to separate the roles of the partners. What it’s lacking is liability protection.

There’s a new type of partnership called a Limited Liability Limited Partnership (LLLP). An LLLP is a limited partnership in the sense that you can differentiate between the partners. But it's limited liability, so if the business gets sued, your personal assets (or your partner’s personal assets) will not be on the line.

It is important to note that just because you’re going into business with a partner or a group of partners does not mean you need to choose one of these types of partnerships. You can also be an LLC or a corporation. There are both single-member and multi-member LLCs. The choice between a partnership and a multi-member LLC often comes down to taxes. If you have narrowed down your choices to these two options, consult a tax professional.

Choosing your business entity type is a very crucial decision for your business and something that will require a lot of thought. As always, do your homework and consult a licensed professional in your state.

The next step in the Legal Checklist for Startups is to Register With Your State.

If you haven’t watched it yet, please check out Step #4 in the Legal Checklist for Startups: Define Your Where. In that section, we talked about making sure you know where you want to register your business. Lyda Law firm is based in Colorado, so we will focus on the process in Colorado. But this process is fairly universal, so the information displayed here should be applicable to your state. As always, if you have any questions regarding the particulars in your state, do your homework and consult a licensed professional.

On the other hand, we’ll tell you a secret about registering with your state. You might not need to pay a lawyer to do it for you.

Let’s walk through the very simple process of how to do it online in Colorado.

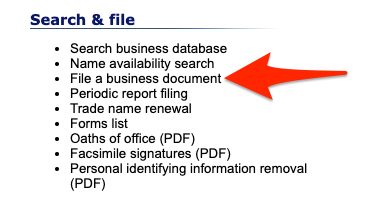

Start by going to the Colorado Secretary of State’s website and navigating to the business section.

If you haven’t already done so, you can search for the availability of your business name. This checks whether somebody has registered your business name in the same state.

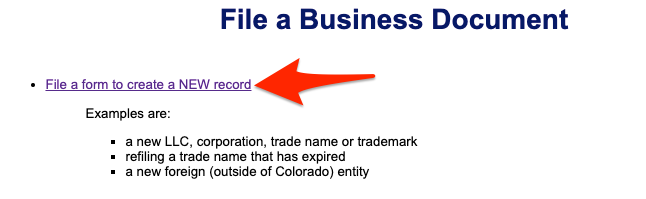

If you’ve already done that, skip ahead to “File a Business Document.” From there, select “File a form to create a NEW record.”

The screen to file a new record allows you to file all sorts of different types of entities; LLCs, partnerships, even socially conscious enterprises like cooperatives and public benefit corporations.

For the purpose of this section, we will an LLC. Note that in Colorado you have to include “LLC” or some version of that phrase in your actual business name. Type our business name and then click next.

That brings up our main form to fill out to register our LLC. Notice that in Colorado the fee is $50.

Start with your physical business address and mailing address.

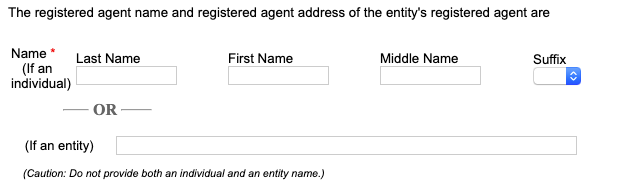

Next, fill in the information for your registered agent. A registered agent is the person who is served with papers if you get sued. Business owners often hire somebody to be their registered agent, but it is something you can do yourself.

Next, verify that the registered agent has consented to being appointed as your registered agent.

For the next step, fill out the information for the person forming this LLC. It’s not totally clear by the language who that is, but a reasonable interpretation is that it is the owner of the business. If you’re a single-member LLC, for example, you’d put in your own name and address

If you are a multi-member LLC, you can add additional members by putting their names and address in a document and attaching it to your form (which comes on the next page).

Now you have to identify the management of the LLC. There are two types of management for an LLC: member-managed or manager-managed. A member-managed LLC means that the member(s) of the LLC is actually managing the company. Manager managed means that you are hiring somebody else who is not a member to manage the company.

Now, you can attach additional information, such as a detailed operating agreement or a list of the other members of the LLC.

If you would like to delay the effective date of your registration, you can do so now.

For the penultimate step, put in your email address so that you can receive notifications when it’s time to update your business information.

Then finally, put in the name and mailing address of the individual causing this document to be delivered for filing. This is different from the person forming the LLC, this is the person (or persons) who is filling out this form.

Then you click submit! After you click submit, you’ll need to enter your payment information to cover the fees associated with registering. Fees vary from state to state, but they are generally fairly reasonable.

As you can see, it is very simple. You can pay a lawyer to do it, or you might be able to get away with doing it yourself. It all depends on your level of comfort.

Now that we’re done with that, let’s move on to selecting your tax treatment.

The next step after registering with your state is to select your federal tax treatment. This is similar to selecting your type of entity, but it is slightly different because the IRS treats your entity differently from how your state treats your entity.

For example, the IRS does not recognize the concept of an LLC, a limited liability company is a state law concept. That means that the IRS does not have a designated way to tax LLCs. So if you register as an LLC with your state, you will then have to decide how you want the IRS to tax your company.

If you are a single-member LLC, the default method of taxation is that the IRS will treat you as a sole proprietor. However, you can elect to be taxed as a subchapter S corporation.

The question of whether to be taxed as a sole proprietor or an S corp is really a financial question. The general rule of thumb is that if your business is a side-hustle and not your primary source of income, then there are potential tax benefits of choosing to be a sole proprietor in the eyes of the IRS. But if your business is your primary source of income, then you may want to register as an S corp.

If you are a multi-member LLC, the default tax treatment will be to treat you as a partnership. But again, if you want to elect to taxed as an S corp, you can do so.

If you choose to be taxed as an S corp, you will not only need to select that option when you obtain your EIN (which we’ll talk about in the next video), but you will also have to fill out and mail in IRS Form 2553 to elect to be taxed as a subchapter S corporation.

Since this is a financial decision, we highly recommend you consult with a local tax professional.

You will also need to make a decision if you are a corporation. The primary options are to be taxed as a C corporation or as an S corporation. We talked about the differences in Step #7: Select Your Entity Type, so we won’t spend too much time on that here. From a taxation perspective, C corps have double taxation, while S corps do not have double taxation.

So that’s selecting your tax treatment. Once again, this is a separate concept from selecting your entity type because the IRS does not recognize LLCs.

Next up, we will talk about obtaining your EIN, or employer identification number, from the IRS.

An EIN is your Employer Identification Number, it’s also commonly known as a tax ID. Your EIN is like the social security number for your business. All it is is a unique identifying number for your business.

If you plan to have employees, you will need an EIN. You also need an EIN to open a separate bank account for your business, which we will cover in the next section.

The main point we want to emphasize in this section is that obtaining your EIN from the IRS is very easy. Depending on your level of comfort, you may be able to do it yourself without the help of a CPA or attorney. As always, make sure to do your homework and assess your own level of comfort.

In this section, we’re going to show you the process of actually going online and obtaining your EIN from the IRS.

If you Google “IRS EIN” you will notice there are tons of sites with .com, .us, or .org URLs. You do not want to go to one of those sites. Make sure you are on the official government website (denoted by the .gov URL).

First off, to apply for your EIN your principal business must be located in the United States or U.S. Territories and you must have a valid Taxpayer Identification Number (SSN, ITIN, EIN). If you have those things, head to this page to begin the application process.

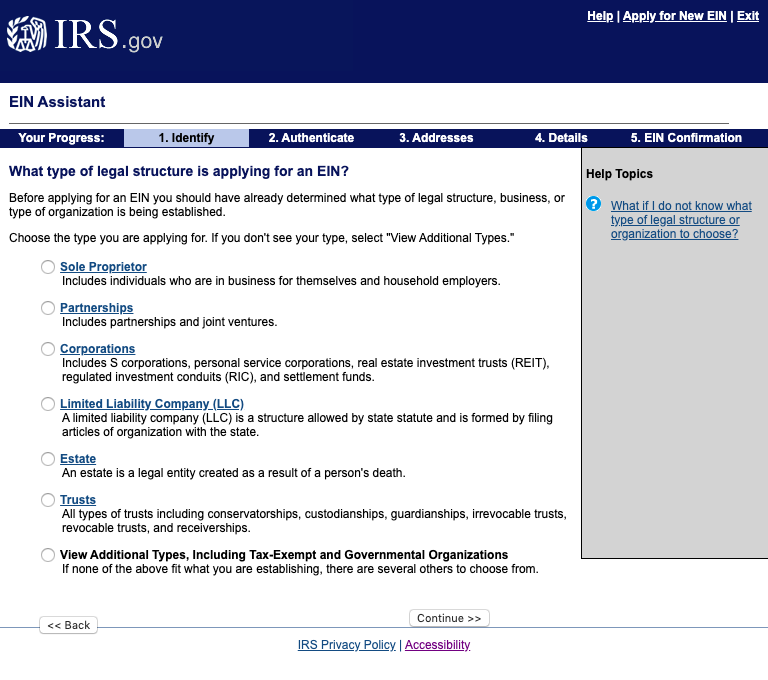

This first section of the application is to select your entity type (which we discussed in Step #7).

After you select your entity type, you will be greeted with a confirmation page that displays more information about your type of entity you selected. When you are comfortable with your selection, you can continue with the application.

After selecting and confirming your entity, you need to express why you are looking to obtain an EIN. If you’re ready this page, your reason is most likely “Started a new business.”

From there, you will have to assign the responsible party of your business, which you will likely make yourself. If you have a third-party apply for your EIN, you will need special permission for them to do so. Please note, you will need to enter your SSN at this time.

The next step is to confirm the physical address of your business. After confirming the address, you will need to supply additional information about your business, make sure the information here matches the information you entered when you registered with your state.

Also, if you enter a trade name, such as a name where you drop the LLC, make sure your trade name is registered (separately) with your state.

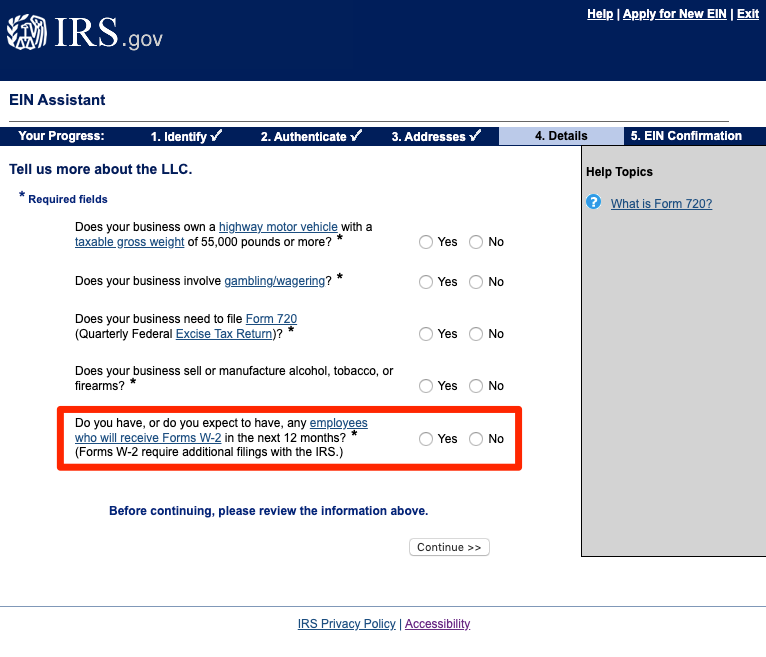

The next page asks about special circumstances that will affect how your business is taxed. The most common circumstance is hiring employees. If your business plans to have any employees within the next year, make sure to make the “Yes” box. If you select “Yes,” the next page will ask you about how many employees you expect to have.

After completing the information about employees, you will have to answer more questions about your type of business. All of the selections are very straightforward. If none of the business types match your line of work, like if you offer a service not listed, you can always check “Other.”

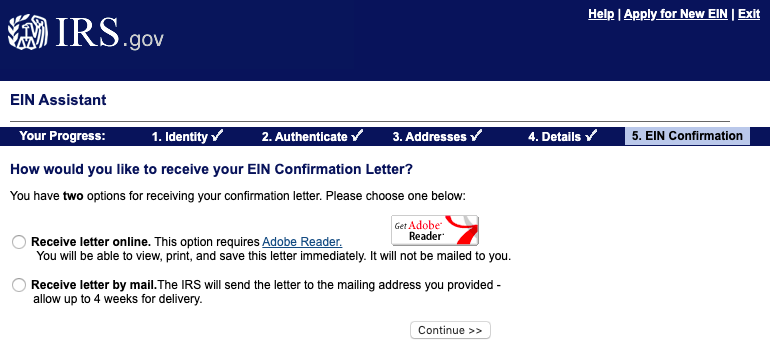

You’re almost done! After confirming information about your product/service, you can select to receive your EIN online. If you select this method, you will receive a PDF immediately with your new EIN.

Congratulations! Now that you have your EIN, you can move onto the next step of the Legal Checklist for Startups: Open a Separate Bank Account for your Business.

Now that you have obtained your EIN from the IRS, you can go now set up a separate bank account for your business.

It is important to have a separate bank account for your business because you do not want to commingle your business funds with your personal funds.

One reason that you do not want to commingle your funds is that if you are sued, your financial records could become part of that lawsuit. That means that you run the risk of airing your personal financial information in open court.

Also, if you commingle funds, an opposing lawyer could potential come after your personal assets in a lawsuit.

You can avoid keeping your personal finances out of a lawsuit, and to reduce the risk of losing your personal assets in a lawsuit, it is best to keep all personal and business transactions separate.

Having a separate bank account for your business is also helpful when you want to show your financials to someone. It is not uncommon for lenders, investors, and even landlords to want to take a look at your finances. This is obviously much simpler if you only have one account to show them.

The same goes for accounting. If you don’t have a separate bank account for your business, it could be a major hassle to go through your financial records every month and categorize transactions line by line.

So for liability, privacy, ease of use, and for accounting reasons you should set up a bank account for your business.

One thing we should mention: if you have already started your business and you have not created a separate account yet, it's not too late. Set up a new account as soon as possible and only use that account moving forward.

How about selecting a bank? Here are a few things to consider.

First off, look for free checking. Obviously free is almost always better, but be aware of hidden fees.

Also, be mindful of your bank’s location. Local banks can be great because they sometimes offer better customer service. But national banks can be beneficial if you travel often for business and need local branches wherever you go.

One option that you should strongly consider is a credit union. Credit unions often support your local community while providing low fees and excellent customer service.

That’s Step #11 in the Legal Checklist for Startups. Next up, we'll talk about determining your industry-specific regulations.

The next step in the Legal Checklist for Startups is to determine your industry-specific regulations.

This is a very complex issue and we would not even be able to scratch the surface of all of the potential regulations for your business. Every business is different and every location is different, so this step is here to flag the issue for you.

In prior sections, such as Obtaining Your EIN or Registering With Your State, we talked about some things that you might be able to do without the help of an attorney. But determining your industry-specific regulations is often too complex to do on your own. For this reason, we highly suggest that you consult an attorney with industry-specific experience.

It is important to ask if they are familiar with your particular line of work because industries can vary wildly in terms of the laws and regulations that govern their conduct. Not only do you have to adhere to state and federal laws, but many industries are also regulated at the state and even county level.

Since we can't mention any specific regulations, let's look at some common things to look out for. First, does your line of work require specific licenses? And does your line of work require specific permits?

Some particular industries that are heavily regulated are:

Many industries may have regulations that you would never think about. For example, if you want to cut hair your state might require a special license.

It is not only important to think about the rules and regulations in your location, but you should also consider the rules and regulations in your customers' locations. If your business involves interstate commerce (the movement of goods or services across state lines), this is definitely something to watch out for.

As you can see, the number of potential regulations is endless. That is why you should consider talking with a licensed professional in your state who has industry-relevant experience.

If you have questions about the regulations that govern businesses in the state of Colorado, send us a message and we should be able to help.

Now that you’ve figured out what rules, regulations and licenses are specific to your line of work, it’s time to determine your potential liabilities and insurance needs.

This is similar to Step #12 because potential liabilities also vary from industry to industry. When we say “potential liabilities,” we are talking about potential risks.

A liability is a risk that you can be held legally responsible for.

For example, if you have a storefront or an office and your customers or clients visit you in that space, there is the potential that they could slip and fall. If a customer hurts themselves in your store, they could potentially sue your business. If they are successful, you could be held legally responsible and forced to cover the cost of the damages of that fall.

When determining your potential liabilities, you need to think about all of the things that could go wrong. It might not be a fun brainstorming exercise, but it is a necessary brainstorming exercise.

During this brainstorm, a few key groups to think about are customers, employees, and competitors. If you have a disgruntled employee, what actions could they take that could negatively impact your business?

You also need to consider the risks that are particular to your type of business. If you work in a potentially dangerous industry, like construction or mining, there are way more risks to consider. Other industries, like anything to do with children, can also be considered very risky.

If you are unsure about how to identify your potential liabilities, you should consult a flat-fee risk management consultant or an attorney.

Consulting with an experienced professional will help you pinpoint potential liabilities that you would never have thought to consider.

In many instances, consulting with a professional can provide you with greater peace of mind. You might sleep better knowing that you've thought about everything that could go wrong with your business and that you've set up the proper protections.

One key facet of being an entrepreneur is managing risk. We’ve already talked about Selecting an Entity Type to manage your risk and limit your liability, but one of the other key ways to limit your liability and manage your risk is to be adequately insured.

If your business has adequate insurance, you will be less impacted financially if you’re found to be legally responsible in a lawsuit. Much like health insurance or car insurance, instead of having to pay “out of pocket,” you can use your insurance to cover the damages.

There are many different types of insurance for business owners. Three common types of insurance policies for business owners are commercial general liability, umbrella, and professional liability.

Commercial General Liability

Commercial general liability policies are the most general type of policy. This type of policy typically covers common business liabilities like if your employee causes damage to property while on the job.

Many business owners make the mistake of assuming that commercial general liability insurance covers just about everything. That is why it is important to make sure you actually read your insurance policy. Do your due diligence and make sure you understand what your policy covers and what your policy does not cover. You might be surprised by what it doesn’t cover.

Umbrella

What if you identify liabilities that your commercial general liability policy doesn’t cover? Or what if your other policy doesn’t cover the full amount? If that happens, you can still get protection through an umbrella policy, which is a type of secondary insurance policy.

A secondary insurance policy only kicks in once you’ve exhausted the limits of your other insurance policies. Umbrella policies are usually cheaper because they are needed less often, but that doesn’t mean you shouldn’t consider purchasing one.

Professional Liability

Professional liability policies protect people in specific professions. The name varies depending on the profession, so you may have also heard professional liability insurance called errors and omissions insurance or malpractice insurance.

If you make a mistake while practicing your profession, professional liability insurance protects you from any lawsuits that seek damages to cover what went wrong.

Professional liability insurance is common among doctors, lawyers, accountants, and real estate agents.

While it is not required to carry professional liability insurance in all states, it can provide peace of mind for both you and for your customers.

There is a huge misconception out there that insurance brokers have the responsibility of telling you what types of insurance you need and how much insurance you need.

That is not the case.

An insurance broker’s primary job is to sell insurance. They are typically paid by commission, meaning there is often the incentive to upsell. That creates a conflict of interest when it comes to suggesting how much insurance you need. The more insurance you buy, the more they get paid.

We’re not saying that people who sell insurance are bad people, we’re just saying that it is not their job to tell you how much insurance you need.

It is your job as a business owner to take a proactive stance on determining your liabilities and figuring out what type of insurance will protect against those liabilities. Once you know what type(s) of insurance you need, it is up to you to select how much protection you need.

As we mentioned earlier, some industries have more liabilities than others, so consulting with a licensed professional in your state can provide some extra peace of mind for your business.

Step #14 in the Legal Checklist for Startups is to Set up an Accounting System for Your Business

Setting up an accounting system is another way to manage your risk as a business owner, because if you let your books get sloppy it could sink your business.

There are two main ways to set up an accounting system:

There are pros and cons of each method.

If you want to do it yourself, your best bet is to use a program like Quickbook or Xero. While these programs do streamline the process, it’s still a time-consuming (and often confusing) task that can take significant time away from your business.

Since accounting is so important for managing your day to day affairs and managing your risk as a business, it’s usually a worthwhile expense to have somebody do it for you. There’s just too much that can go wrong if you try to do it yourself.

The good thing about doing it on your own is that you’ll have a much closer connection to your financials.

That leads us to the second option: hiring somebody to handle your books for you. As you can imagine, there is no shortage of bookkeepers and accountants who you can pay to look after your books.

The biggest pitfall of hiring another person to handle your books is that you could become disconnected from your business’s finances. You never want to let that happen. Losing track of your business’s financials is a surefire way to sink a new business.

If you choose to hire someone to do your bookkeeping for you (which is generally a very good idea), you still need to exercise adequate oversight of that person.

It’s very important that you hire somebody who can give you to-the-minute access to your financials. Programs like Quickbooks Online make this relatively easy.

A credential to look for when hiring an accountant is the CPA credential. CPA’s must pass a certification test, meaning that the state has deemed that person adequate to manage your books.

Just to give you a very basic overview of what an accounting system does, an accounting system breaks your money down into various categories. The important categories for business owners include accounts receivable and accounts payable.

Accounts receivable are funds that you have earned but not yet been paid on. In short, it is money that you are owed. If you’ve shipped your goods or performed your service and not yet been paid, that money is kept track of in accounts receivable.

Accounts payable is just the opposite - money that you owe to others (vendors, service providers, etc.). This is essentially unpaid bills.

Accounting systems also provide profit and loss statements and balance sheets. These two documents can give you a snapshot of your business’s financial health. They are also important because many lenders and investors will want to see a balance sheet before lending money or investing in your company.

Now that you’ve laid down the basic foundation for your business and reviewed your needs, it’s time to put your plan into motion. But before you go out and start setting up relationships with clients, vendors, and employees, you need to complete Step #15 in the Legal Checklist for Startups: Set up Your Basic Contracts.

First off, what is a contract? A contract is just an exchange of promises between two parties.

If you’re not sure if you need a contract, think about if you are exchanging promises. Are you promising to provide them with something and are they promising something in return. If so, you probably need a contract.

An example would be a contract with a client if you are a service provider. In that relationship, you are promising to provide a service and your client is promising to pay you for that service.

Why are contracts important?

A contract is important because miscommunication can happen so easily. In most states, oral contracts are binding. However, anytime you’re exchange promises with another party in your business, it is prudent to get it in writing. Putting your promise in writing (in a contract) will reduce or eliminate miscommunications. Contracts should create clear outlines of what is expected from both parties.

In addition to miscommunication, people sometimes break promises. Contracts give you a way to enforce a broken promise. For instance, if you provide a service and your client doesn’t pay you, you can pursue legal actions to collect on that payment. Having a contract in place will make the legal process much simpler.

Human relations and business relations rely on a certain amount of trust. Contracts help protect you if that trust is misplaced.

Now that you understand what a contract is and why they are important, let’s talk about the basic types of contracts your business might need. But first, please note that basic contracts can be industry-specific, so make sure to do your homework and consult a licensed professional in your state.

To figure out what types of contracts you need, we suggest you go back and review the section on Defining Your “Who.”

In that section, we spend a lot of time discussing business partners. If you are going into business with a partner, it is imperative that you have a contract. Many partnerships exist with unspoken agreements or handshake agreements, get those agreements in writing to make them more enforceable.

In that section on Defining Your “Who,” we also talked about who is going to work for your business. In some instances, it might make sense to have contracts with your employers. It’s also important to have contracts with your independent contractors. Other parties that work for your business include vendors. When working with established vendors, they usually have standard contracts for all of their partners.

And as we mentioned before when talking about providing a service for your clients, you may also need contracts with your customers. Again, the type and substance of that contract will vary greatly depending on what type of business you are in.

Another very common type of contract is an insurance policy. An insurance policy is a contract between you and the insurance company. You are promising to pay your premium and the insurance company is promising to pay out a claim for a covered loss.

The last really common type of contract that we will highlight for you is a lease. Commercial leases can be extremely complicated and they are often written by the landlord, not by the tenant. Since they are usually drafted by the landlord, they often heavily favored the landlord rather than the tenant.

In many cases, the other party will provide contracts and ask you to agree to the terms outlined in that contract. Such is the case with vendors, landlords, and insurance companies. If you are presented with a contract, it is your responsibility to review it, understand it, and negotiate (if needed).

In other cases, you will have to provide the contract. This is very common if you are hiring independent contracts or bringing on clients.

How do you draft your own contracts?

There are some online resources, like LegalZoom and Rocket Lawyer, where you can download basic boilerplate contracts. That is usually the cheapest way to create a contract without having to handwrite it yourself from scratch (which we don’t recommend). The problem with online boilerplate contracts is they are not specific to your business. We’ve talked about this a lot in this checklist, but to reiterate: every business is different. That means the needs of every business are different. A boilerplate contract might not cover everything you need, leaving you legally exposed.

You can also hire an attorney to draft your contracts for you. This can get expensive, so we recommend that you discuss your budget with your attorney before starting. Alternatively, you can seek out a flat-fee law firm with transparent pricing.

If you already have a contract, whether you downloaded it from a legal website, wrote it yourself, or it was presented to you by a landlord or a vendor, you can ask an attorney to review it.

One important thing to note, even if you have a lawyer write or review your contracts, it’s still your responsibility to read and understand what’s in the contract. The lawyer can highlight legal issues for you, but a contract is ultimately a business decision. You, as the business owner, are the one exchanging promises in the contract. So you need to make sure that you’re ok with all of the promises that are exchanged in that contract.

You’ve made it to the final step! Step #16 in the Legal Checklist for Startups is to Keep it Simple.

We appreciate that there is some irony in saying “keep it simple” at the end of a long series telling you all the steps that you need to take (just from the legal perspective) to start your business.

However, it is important to keep it simple.

Once you’ve taken the basic steps to set up your business, and after you’ve sufficiently protected yourself from a legal standpoint, it’s important to focus on your actual business.

Consulting with an attorney can be a great way to help you figure out whether you are properly managing your potential risks so that you can focus on the actual substance of your business. This checklist should also help you identify areas that you may have overlooked.

But don’t underestimate the value of simplicity in starting a business.

In the book The Lean Startup, author Eric Ries makes a great analogy about simplicity in business. He says that when you take your daily commute to work, you really a thousand little decisions. You decide where to turn, when to slow down at a stoplight, whether to speed or take your time. But you make those decisions as you go. You don’t plan out every single decision in advance.

That’s one end of the spectrum.

The other end of the spectrum is launching a rocket ship. Rocket scientists have to plan every single contingency and every single step in the launch of a rocketship.

It’s the equivalent of trying to make every decision for morning commute before you even get in the car. The difficult part here is that there are so many variables and you don’t know what will happen once you’re behind the wheel.

Rocket scientists have to account for every single variable beforehand and determine ways to navigate every single obstacle before the rocket takes off.

Eric Ries says that starting a business is, and should be, more like your daily commute. Too many business owners treat starting a business like launching a rocket ship. But the fact is, you don’t know what’s going to happen. You will need to navigate obstacles as they come up, and that’s okay.

Make the minimum number of decisions that you can now, think through your end goal and the potential contingencies in all of that. But don’t let planning get in the way of actually starting.

Once you have gone through this checklist, be sure to consult with a licensed professional in your state to ensure you properly set up your business in accordance with local law.

When you're ready to take the plunge, contact our team of startup and small business attorneys to see how we can help you start, manage, or grow your business.

If you have legal insurance, please call 844.844.LYDA (844.844.5932)

844.844.9400

Denver:

5335 W. 48th Ave.

Ste. 501

Denver, CO 80212

855.855.9400

Los Angeles:

11845 W. Olympic Blvd.

Suite 1100W

Los Angeles, CA 90064

Santa Clarita:

28338 Constellation Road

Ste. 900

Santa Clarita, CA 91355

833.822.9400

Weston:

2200 N. Commerce Parkway

Suite 200

Weston, FL 33326

833.822.9400

Kansas City:

7280 NW 87th Terrace

Kansas City, MO 64153

Serving rest of Missouri remotely

833.822.9400

Nashville:

40 Burton Hills Blvd.

Ste. 200

Nashville, TN 37215

833.833.9400

Austin:

2105 E. MLK Blvd. #109

Austin, TX 78702

Permian Basin & Monahans:

201 E. 4th St.

Monahans, TX 79756

855.855.9400

Seattle:

450 Alaskan Way South, Suite 200

Seattle, WA 98104